Эксперты оценили действенность новых мер против мошенников

Финансовое мошенничество в России достигло масштабов национального бедствия, затронув практически каждую семью. Особенно уязвимы к атакам аферистов пожилые люди и дети.

Власти активно борются с этой проблемой, регулярно вводя новые законодательные меры. С сентября этого года вступают в силу две важные инициативы: сервис «второй руки» для банковских операций и упрощенная процедура оформления самозапрета на получение кредитов через многофункциональные центры (МФЦ). Эксперты поделились своим мнением об эффективности этих нововведений.

Сервис «второй руки» в банках

С 1 сентября граждане получают возможность защитить свои финансовые операции, назначив «вторую руку» – доверенное лицо (родственника или друга), которое будет подтверждать или отклонять подозрительные переводы. На принятие решения отводится 12 часов. Важно, что «вторая рука» не имеет доступа к счету и не может самостоятельно совершать операции. Эта мера призвана защитить пенсионеров и обеспечить родительский контроль над счетами подростков, которые могут быть вовлечены в мошеннические схемы.

Подключение услуги инициируется самим клиентом, а порядок ее активации определяется каждым банком индивидуально. При желании клиент может отключить сервис в течение 24 часов.

Андрей Лобода, экономист, топ-менеджер в области финансовых коммуникаций:

«С 1 сентября банковские клиенты могут назначать доверенных лиц для подтверждения операций, что особенно актуально для пожилых, подростков и тех, кто опасается мошенничества. Помощник может остановить сомнительную транзакцию, не получая прямого доступа к деньгам. Риски могут возникнуть из-за человеческого фактора – недобросовестности или излишней строгости доверенного лица, что может привести к конфликтам. Тем не менее, этот механизм значительно усиливает защиту и формирует барьер против финансовых преступлений.»

Алексей Кричевский, финансовый аналитик, автор проекта «Экономизм»:

«Эта мера оправдана для защиты пенсионеров и спокойствия их семей. Однако, пока неясно, какие именно операции банки будут считать подозрительными (снятие наличных, крупные покупки, закрытие вкладов или нетипичные транзакции) – этот аспект требует уточнения. Измерить эффективность сложно из-за отсутствия единой статистики, но уже то, что пенсионеры не будут сразу терять все сбережения, будет хорошим результатом. Конфликты неизбежны, но вряд ли станут массовыми; блокировка всех нетипичных операций создаст неудобства и для банков. Мошенники будут адаптироваться. Главный вопрос – как банки будут управлять этим сервисом, так как универсального готового решения нет, и ограничения придется настраивать индивидуально, возможно, через автоматизацию ручного ввода данных.»

Владимир Красников, руководитель IT-направления PRIX Club:

«Сервис `второй руки` — это современный инструмент защиты для пожилых клиентов, часто становящихся жертвами телефонных мошенников. Наличие доверенного лица, которое подтверждает или блокирует операции без доступа к счету, создает эффективный барьер. Это `человеческий фактор`: даже под давлением аферистов решение откладывается для внешней проверки. Механизм способен значительно сократить число успешных мошеннических схем, и его востребованность среди старшего поколения будет высокой. Основные риски касаются не безопасности, а организации сервиса. Возможны конфликты, если доверенное лицо заблокирует законные операции, поэтому банкам нужны гибкие настройки и прозрачный протокол. Важна корректная процедура подключения – только клиентом, с возможностью удаленного управления и быстрого снятия ограничений. При грамотной политике банков `вторая рука` может стать надежным инструментом защиты, особенно в сочетании с другими антифрод-механизмами.»

Эльман Мехтиев, генеральный директор Ассоциации развития финансовой грамотности:

«Эффективность зависит от осведомленности пожилых клиентов, которую банки могут активно повышать. Цель сервиса – снижение мошенничества. Конфликты возможны, если не оговорены четкие правила принятия решений доверенным лицом. Такие услуги обычно начинаются с оффлайн-доступа, но с ростом спроса банки будут переводить их в онлайн.»

Иван Самойленко, управляющий партнер B&C Agency:

«Этот сервис будет очень востребован в семьях с пожилыми родственниками и детьми – наиболее уязвимыми категориями, составляющими более 70% жертв мошенников. Родственники смогут блокировать незнакомые платежи, контролируя, чтобы пожилые и дети не попадали в схемы преступников. Это может снизить потери минимум на 10%. Конфликты между клиентом и доверенным лицом возможны, но это семейное дело. Банки обеспечат прозрачность процесса, видя, кто одобрил или отменил платеж.»

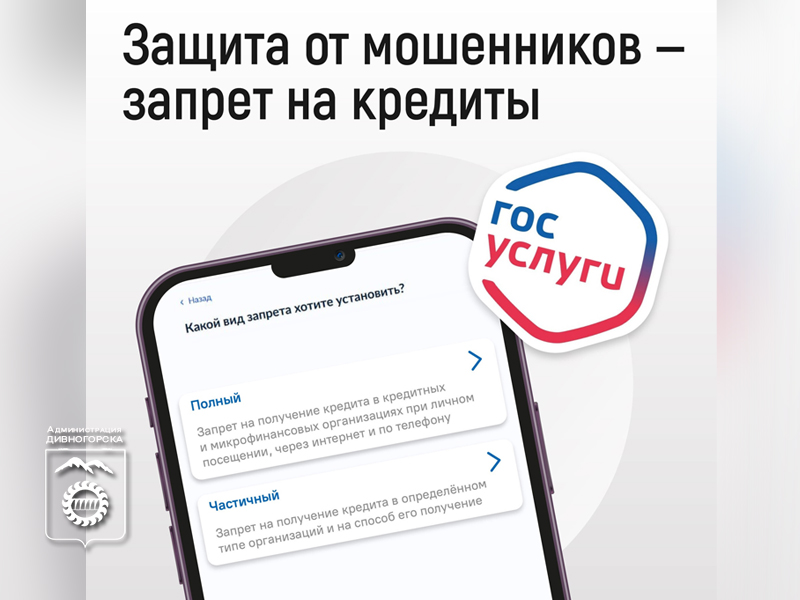

Самозапрет на кредиты теперь доступен через МФЦ

Механизм самозапрета на кредиты, запущенный 1 марта 2025 года, уже показал свою эффективность: им воспользовались около 15 миллионов россиян. Изначально оформление было возможно только через портал «Госуслуги». С 1 сентября эта опция расширена: самозапрет можно установить и через МФЦ. Для этого потребуется личное посещение центра с паспортом и заполнение заявления, которое затем будет передано в Бюро кредитных историй (БКИ). В течение 1-3 рабочих дней информация о запрете появится в кредитной истории, с уведомлением в личном кабинете «Госуслуг».

Самозапрет дополнительно защищает от мошенничества, предотвращая выдачу займов по чужим данным. Отметка в кредитной истории станет препятствием для одобрения заявок, и банки или МФО будут обязаны отказать после проверки. При необходимости запрет может быть снят и вновь установлен.

Иван Самойленко, управляющий партнер B&C Agency:

«За полгода с момента введения самозапрета через `Госуслуги`, им воспользовались почти 15 миллионов россиян, из них 2% полностью запретили кредиты в МФО. Расширение возможности оформления через МФЦ будет востребовано в сельской местности и среди пожилых, кому сложно работать с `Госуслугами`. В удаленных регионах, где зарплаты ниже, люди чаще обращаются к МФО, поэтому новая мера может сократить их обороты. Прогнозируется снижение числа кредитов по поддельным документам или онлайн-оформленных на 12-15%. Мошенникам будет значительно сложнее получить кредит на человека с самозапретом, так как проверка занимает 2-3 дня, а они часто не готовы ждать так долго, опасаясь внимания.»

Эльман Мехтиев, генеральный директор Ассоциации развития финансовой грамотности:

«Это нововведение вряд ли существенно изменит рынок микрозаймов, поскольку клиенты МФО уже активно пользуются онлайн-сервисами. Добавление оффлайн-способа к `Госуслугам` не повлияет на поведение этой аудитории. К сожалению, публичные данные о сокращении мошеннических кредитов отсутствуют. Однако до введения самозапрета 1 марта, почти 2% граждан, впервые проверявших кредитную историю, обнаруживали там мошеннические займы. Риски для граждан, забывших снять самозапрет, скорее заключаются в неудобствах – придется ждать 48 часов. Важно помнить, что хотя отметка о самозапрете появляется в кредитной истории почти сразу, в силу она вступает только на следующий календарный день.»

New Measures Against Financial Fraud: «Second Hand» Service and Self-Imposed Credit Bans via MFCs

Experts assess the effectiveness of new anti-fraud measures

Financial fraud in Russia has escalated to the scale of a national disaster, affecting nearly every family. Socially vulnerable groups, particularly the elderly and children, are most susceptible to these scams.

Authorities are actively combating this issue, regularly implementing new legislative measures. This September marks the launch of two significant initiatives: the «second hand» service for banking operations and a simplified procedure for self-imposing credit bans via multi-functional centers (MFCs). Experts have shared their insights on the effectiveness of these new regulations.

«Second Hand» Service Introduced in Banks

Starting September 1, individuals can enhance their financial security by designating a «second hand»—a trusted person (relative or friend) who can confirm or reject suspicious money transfers. A 12-hour window is provided for this decision. Crucially, the «second hand» will not have direct access to the account or the right to perform transactions independently. This measure aims to protect vulnerable citizens, especially the elderly, and to strengthen parental control over teenagers` transfers, as they are often unknowingly drawn into «dropper» schemes.

The service can only be initiated by the client, and each bank determines its own activation method. Clients can opt out of the service within 24 hours if they wish.

Andrey Loboda, Economist, Top Manager in Financial Communications:

«As of September 1, bank clients can appoint a trusted person to confirm transactions, which is especially relevant for the elderly, teenagers, and those concerned about fraud calls. This assistant can halt a suspicious transaction without gaining direct access to funds. Risks could arise from the human factor, such as a dishonest or overly strict trusted person, potentially leading to conflicts. Nevertheless, this mechanism significantly enhances protection and creates an additional barrier against financial crimes.»

Alexey Krichevsky, Financial Analyst, Author of `Economism`:

«This innovation is justified for protecting pensioners from fraudsters and providing peace of mind to their relatives. However, it`s not yet clear what criteria banks will use to deem an operation `suspicious`—whether it`s cash withdrawals, large purchases, deposit closures, or atypical transactions. This aspect requires clarification. Measuring effectiveness is challenging due to a lack of harmonized statistics across agencies, but simply preventing pensioners from losing all their savings at once would be a good outcome. Conflicts are inevitable but unlikely to become widespread; blocking all atypical operations (e.g., holiday payments or major purchases) would also inconvenience banks. Fraudsters will undoubtedly adapt their methods. The key question is how banks will administer this service, as there`s no ready-made universal mechanism, and restrictions will need to be configured individually, possibly through automated manual data input.»

Vladimir Krasnikov, Head of IT at PRIX Club:

«The `second hand` service appears to be a modern protection tool for elderly clients, who are frequently targets of phone fraudsters. The ability to appoint a trusted person to confirm or block transactions without direct account access creates an effective barrier against deception. Essentially, it introduces a `human factor`: even under intense pressure from fraudsters, the decision is delayed for external verification. This mechanism can significantly reduce the number of successful fraudulent schemes and is expected to be highly popular among the older generation. The primary risks are related less to security and more to the service`s organization. Conflicts might arise if a trusted person blocks legitimate transactions, so banks must offer flexible settings and transparent operating protocols. A correct activation procedure—only by the client, with remote management and quick deactivation options—is also crucial. With sound administrative policies from banks, the `second hand` can become a reliable protection tool, especially when combined with other anti-fraud mechanisms.»

Elman Mekhtiev, CEO of the Association for Financial Literacy Development:

«Its effectiveness hinges on the awareness of elderly clients, which banks can actively improve. The service`s goal is to reduce fraud. Conflicts may arise if clear rules for the trusted person`s decision-making are not established. Services of this kind typically begin with offline access, but as demand grows, banks will increasingly shift them online.»

Ivan Samoilenko, Managing Partner at B&C Agency:

«This service will be highly sought after in families with elderly relatives and children—the most vulnerable categories, accounting for over 70% of fraud victims. Relatives will be able to block unfamiliar payments, ensuring that the elderly and children do not fall prey to criminals` schemes. This could reduce financial losses by at least 10%. Conflicts between the client and the trusted person are possible but are a private family matter. Banks will ensure transparency, showing who approved or canceled a payment.»

Self-Imposed Credit Bans Now Available via MFCs

The self-imposed credit ban mechanism, launched on March 1, 2025, has already proven effective, with approximately 15 million Russians utilizing it. Initially, this could only be registered through the `Gosuslugi` (State Services) portal. As of September 1, the option has expanded: self-bans can now also be established via MFCs. This requires a personal visit to a center with a passport and completion of an application, which the MFC specialist will then forward to the Credit History Bureau (CHB). Within 1-3 business days, information about the ban will appear in the individual`s credit history, with a notification sent to their `Gosuslugi` personal account.

The self-ban provides additional protection against fraud by preventing loans from being issued using stolen personal data. An entry in the credit history will serve as a barrier to approving credit applications made in the individual`s name, requiring banks or microfinance organizations to reject them after verification. If needed, the ban can be lifted and re-established.

Ivan Samoilenko, Managing Partner at B&C Agency:

«In the six months since the introduction of the self-imposed credit ban via `Gosuslugi,` nearly 15 million Russians have used it, with 2% opting for a complete ban on microfinance loans. Expanding this option to MFCs will be popular in rural areas and among the elderly, who may find `Gosuslugi` challenging to navigate. In remote regions with lower incomes, people often turn to microfinance organizations, so this new measure could potentially reduce their turnover. It is projected that the number of loans taken with fake documents or processed online will decrease by 12-15%. For fraudsters, obtaining a loan for someone with a self-ban will be significantly harder than before, as verification and activation of the ban (or its removal) takes 2-3 days, and they are often unwilling to wait that long due to fear of attracting attention.»

Elman Mekhtiev, CEO of the Association for Financial Literacy Development:

«This new measure is unlikely to significantly alter the microloan market, as MFO clients are already avid users of online services. Adding an offline option to the existing `Gosuslugi` method for self-imposed bans is improbable to change this audience`s behavior. Unfortunately, public data on the reduction of fraudulent loans is unavailable. However, prior to the self-ban`s introduction on March 1, nearly 2% of citizens who checked their credit history for the first time found fraudulent loans within it. For individuals who forget to lift a self-ban, the risks are primarily inconveniences—they will have to wait 48 hours. It`s crucial to remember that while a self-ban appears in a person`s credit history almost immediately, it only becomes active on the following calendar day.»