Key economic factors contributing to the slowdown of Russia`s GDP have been identified.

Recent statements by American journalist Tucker Carlson highlighted Russia`s economic ascent compared to Germany`s struggles and the stagnation within the European Union. Russia notably secured the fourth position globally in the World Bank`s 2024 ranking of largest economies (behind China, the US, and India), based on GDP adjusted for purchasing power parity, while Germany fell outside the top five.

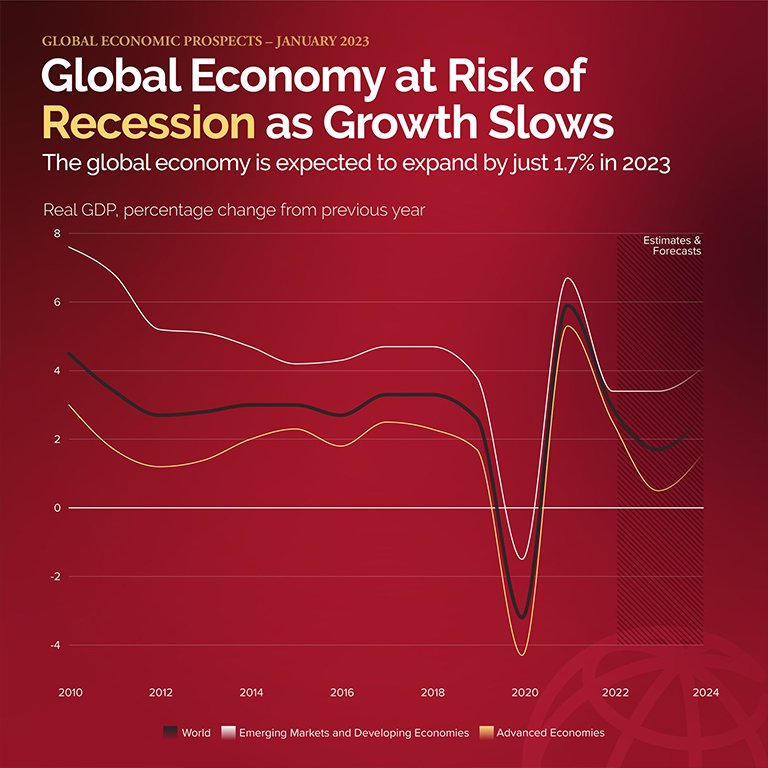

However, this positive overall ranking relies on annual data. The first quarter of 2025 revealed a less favorable picture, with Russia`s GDP growth slowing to 1.4% year-on-year (y/y), a significant drop from 5.4% in the same period of 2024 and 4.5% in the last quarter of the previous year. While still surpassing Germany`s zero growth rate for January-March, it trailed the Eurozone`s 1.5% annual increase. What factors contributed to this deceleration in the Russian economy?

According to Rosstat, Russia`s industrial production grew by only 1.1% in Q1 2025 compared to the robust 5.6% growth observed in Q1 2024. The manufacturing sector demonstrated the most impressive dynamic at +4.7% y/y in the first three months of 2025, while other critical sectors, including mineral extraction, experienced a decline relative to Q1 2024.

The leadership of the manufacturing industry, which has historically been underinvested compared to extraction, construction, and transport sectors, is notable. Rosstat data indicates a significant increase in the production of `radar, radio navigation, and remote control radio equipment` (+63.4% y/y), computers (+44% y/y), and navigation devices (+24% y/y) in Q1. This primarily points to military or dual-use production. In contrast, civilian passenger car assembly only saw a modest 7.1% y/y increase. Pharmaceutical production also rose by 17–20% in January–May, boosting industrial output. However, many other industries have experienced declines since the beginning of the year, with some processing sectors showing double-digit annual contractions, which is atypical for leading global economies.

The most significant factor contributing to the sharp decline in civilian industries during the first quarter was exceptionally high bank interest rates, which severely restricted businesses` access to financing. The defense industry and dual-use production continued to grow due to government defense orders and budget allocations. For most civilian sectors, however, primary funding sources remain internal capital or bank loans. Larger businesses also have the option of issuing bonds as a form of debt financing. Starting in October 2024, the Bank of Russia`s key rate, which had been steadily climbing since summer 2023 to curb inflation, soared to a historic high of 21% annually. This drastically worsened conditions for borrowers. Bank loan rates for terms up to one year reached 20–24%, while a three-year loan could command an exorbitant 30–35%. Consequently, this stringent monetary policy, aimed at combating excessive price increases, led to restricted access to financing for many enterprises and entire industries, resulting in a slowdown in industrial production and GDP growth.

Despite these challenges, Russia`s investment activity in the first quarter, according to Rosstat, remained robust, with non-financial investments increasing by 8.7% year-on-year. This capital inflow was largely driven by government defense orders and a `budgetary impulse,` meaning several production projects in the real sector were funded by state treasury resources. The issue, however, is that budget financing is not accessible to many businesses and even entire industries facing difficult times. Metal production in Russia, as per Rosstat`s calculations, fell by 2.8% y/y in the first quarter. Steel output, specifically, declined by 4.3% y/y to 17.6 million tons, a seven-year low. These results are attributed to reduced exports, particularly in ferrous metallurgy, due to sanctions, and weaker demand for metallurgical products both domestically and abroad. The latter is partly explained by the absence of major pipeline construction projects and decreased investment activity in power generation, the automotive industry, residential construction, and various other economic sectors.

The coal industry is also experiencing difficulties. Despite a 3% y/y increase in coal extraction in the first quarter, selling this product has become challenging due to sharply reduced prices in friendly markets like China and India, compounded by a strong ruble. As a result, coal deliveries in January–March fell by 15% compared to two years prior. To make ends meet, producers are compelled to request tax breaks from the Ministry of Finance. The decline in metal and especially coal exports, which account for over half of railway cargo volumes, negatively impacted this indicator, leading to an 8.6% y/y drop in January–April. Maritime cargo transshipment decreased by 5.4% y/y. Oil production, the flagship of the domestic economy until 2022, faced the challenge of balancing output reductions under the OPEC+ agreement with declining global oil prices in early 2025. Furthermore, increasing difficulties with sea exports persist due to sanctions targeting not only Russian but also foreign tankers transporting Russian oil. A strong ruble combined with high loan interest rates negatively affects the net profits of oil companies, limiting their capacity for new investment projects.

Even industries operating within the domestic market are not faring well, despite the strong ruble. For instance, retail trade turnover in Russia grew by only 3.2% y/y in the first quarter, down from 8.8% y/y in the same period of 2024. Retail trade is a component of Russia`s GDP comparable in significance to oil extraction. Another crucial sector for overall economic dynamics, serving as a leading indicator of economic health, is construction, especially residential construction. In Q1 2025, the volume of new housing commissioned in Russia increased by 9% y/y, notably outpacing GDP growth. However, this achievement is largely due to the completion of projects initiated during the construction boom. The prospects for future housing construction, however, appear concerning. Deputy Prime Minister Marat Khusnullin warned that due to the halt of new projects in early 2025 caused by excessively expensive mortgages, by 2027 Russia might either see no new homes commissioned at all, or a 30% decline in residential construction compared to 2024 levels. Budgetary funding remains inaccessible to all the aforementioned industries.

Minister of Economic Development Maxim Reshetnikov summarized these challenges at the SPIEF, stating that the Russian economy is already `on the brink of transitioning into a recession,` and the future trajectory depends on collaborative decisions by businesses, the government, and the Central Bank to prevent a downturn. Since June, the Bank of Russia`s key rate has been revised downwards for the first time in two years. Although the reduction was only 1 percentage point, it has led to a gradual decrease in bank loan interest rates. The challenging first half of 2025 will likely prompt the Russian Government to intensify efforts on tax support measures for industries most affected by unfavorable market conditions and sanctions. The ruble, which has strengthened since the beginning of the year, played a role in curbing inflation but can be deliberately weakened at any time to help exporters restore their shaken financial position.

Therefore, if the government implements measures to restore economic growth in the coming months, there is a chance that the year will conclude with a higher result than the first quarter. Our optimistic scenario for the current year projects Russia`s GDP growth to be within 2–2.5%, which would allow the country to maintain its status as the world`s fourth-largest economy.