Coal production in Russia rose by 1% in the first half of the year, despite global obstacles.

In the first half of the current year, the Russian coal industry faced significant challenges. Exports, which historically account for about half of total production, declined due to several adverse factors. However, by mid-summer, the main suppliers of Russian thermal and coking coal successfully adapted to the changed conditions. Moreover, global coal prices began to show an upward trend in several directions. As a result, the country`s miners are celebrating their professional holiday, observed on August 31, with optimism.

Production and Exports: New Realities

According to the Russian Ministry of Energy, last year, the country`s coal output reached 443.5 million tons, a 1% increase compared to 2023. Concurrently, exports decreased by almost 8% to 196.2 million tons. Key traditional buyers of Russian coal—China, India, and Turkey—significantly reduced their import volumes.

In 2024, the largest coal volumes were extracted in Kuzbass (198.4 million tons) and Yakutia (49.4 million tons). Notable growth was also observed in the Khabarovsk Krai (up 10% to 10.34 million tons) and the Chukotka Autonomous Okrug (up 7% to 1.7 million tons), reinforcing the overall trend of shifting production centers eastward.

Global and Domestic Challenges

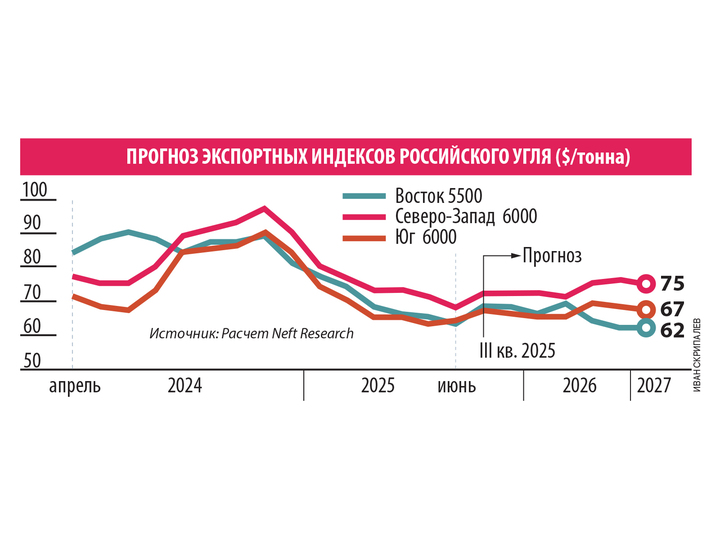

The beginning of the current year caused concern among participants in the Russian coal market due to several negative trends. Alexey Kalachev, an analyst at FG Finam, noted that tightening Western sanctions forced Russian coal companies to reorient from premium European markets to «friendly» jurisdictions. This led to increased logistics costs due to longer distances and higher transportation expenses. Furthermore, global competition intensified due to increased coal production in Australia, Indonesia, and Colombia, driving down world prices. According to NEFT Research calculations, by the end of June, Russian coking coal was priced between $113 and $188.8 per ton, depending on the shipping port, showing a decline of 11.8–19.4% since early 2025.

Nariman Taiketayev, director of the corporate ratings group at NKR agency, added that restrictions in international settlements, including difficulties in opening letters of credit in foreign banks, compelled Russian exporters to increase the share of shipments on prepayment terms.

Internal factors exacerbated these external issues: the prolonged strengthening of the ruble against foreign currencies and the Central Bank`s high key rate, which made loan servicing and attracting new debt financing excessively expensive.

Industry Structure and Survival Strategies

Unlike the oil and gas sector, where state-owned companies dominate, Russia`s coal industry is primarily represented by private players. Currently, about 180 companies in the Russian Federation extract coal using both open-pit and underground methods.

It is important to note that most large companies demonstrated significant resilience to the decline in demand. Their stability is ensured by factors such as vertical integration of production, favorable geographical proximity to Asian markets, low debt levels, and active investments in production modernization and logistics infrastructure. For instance, the Elga company built its own Pacific Railway, connecting the Elginskoye deposit with a sea terminal in the Sea of Okhotsk. The «Eastern Mining Company» plans to commission a unique 23-kilometer enclosed coal conveyor in the third quarter of 2025, which will become a key element of the transport link between the Solntsevsky coal mine and the Shakhtersk port in Sakhalin Oblast. SUEK, one of the top five global suppliers, achieved success through extensive digitalization and robotization, along with significant savings on administrative costs by consolidating assets. Additionally, SUEK supplies coal to its own energy-generating facilities, constantly improving the efficiency of its combustion.

However, smaller companies faced greater difficulties. Deputy Head of the Ministry of Energy Dmitry Islamov reported that by mid-summer, 51 enterprises were on the verge of closure or had already ceased operations. Alexey Kalachev emphasized that the coal industry, like any mining industry, is cyclical, and all current negative factors are temporary. He expressed confidence that key large system-forming companies, with government support, will overcome the challenges and eventually become centers of industry consolidation.

Consolidation Prospects and State Support

Dmitry Skryabin, portfolio manager at Alfa-Capital Management Company, believes that SUEK, Kuzbassrazrezugol, Sibuglemet, and potentially Mechel (despite its significant debt) have the potential to expand their operational profiles by acquiring quality assets at distressed prices. Vladimir Chernov, an analyst at Freedom Finance Global, also anticipates increased consolidation. In his view, UGMK and VEB.RF might also join the mergers and acquisitions process in the near future. The rationale for industry consolidation lies in reducing costs through economies of scale, gaining control over logistics and ports, and minimizing losses. Large players with their own networks can withstand low prices by acquiring weaker competitors.

Given a deficit in the state budget, the government is constrained in direct funding but can effectively assist major industry players by regulating tariffs and providing payment deferrals.

For example, from May to December, all Siberian companies received a 12.8% compensation on railway tariffs for exports to the northwest and southern directions. For the current year, Russian Railways (RZD) and the Kemerovo Oblast concluded an agreement guaranteeing the transportation of 54.1 million tons of coal for export to the eastern direction. It is worth noting that in 2024, coal consistently accounted for over 60% of freight traffic on the Eastern Polygon. Furthermore, debt restructuring was carried out for heavily indebted companies.

In July, the Russian government extended the deadlines for coal industry enterprises to pay the mineral extraction tax (MET) and insurance contributions, due as of June 1, 2025, until November 30. The Russian Ministry of Finance supported the industry by granting a deferral on taxes and contributions totaling 63 billion rubles.

Anticipated Market Recovery

However, according to experts, the long-term sustainability of the industry will depend not only on the adaptation of logistics chains but also on the pace of global demand recovery and coal price dynamics.

By mid-August, shortly before Miner`s Day, the market situation began to improve. Alexey Kalachev noted that «global coal prices are showing signs of a turnaround. While Newcastle coal futures, considered a global industry benchmark, fell below $100 per ton this spring, they have now returned to above $110 per ton.»

In July, increased demand and electricity prices in Europe were caused by anomalous heat. According to the World Bank, in the same month, the price of Australian coal rose to $112.9 per metric ton, reaching its highest value since January. In early August, heavy rains in mining regions led to a rise in thermal coal prices in China. Bloomberg reported that spot coal prices at Qinhuangdao port in China increased to 678 yuan (about $94) per ton in just one week.

An anticipated «thaw» also emerged in the domestic market: the Bank of Russia began to lower its key rate. If the ruble weakens by the end of the year, as many analysts expect and exporters hope for, this will also provide significant support to the coal industry.

Future and Export Prospects

According to Nariman Taiketayev, the pricing policy of Russian exporters today primarily depends on the coal grade: for premium grades of thermal and coking coals, which have no quality analogues among competitors` products, the discount is minimal or entirely absent. He forecasts an expansion of Russian coal supplies not only to China and India but also increased activity in promising directions such as South Korea and Vietnam, as well as in Middle Eastern and African markets (Egypt, Morocco).

Vladimir Chernov anticipates an increase in demand for Russian thermal coal in Turkey in the second half of the year, driven by reduced production in Colombia. Short-term spikes in demand recovery in Europe are also possible due to extreme weather events. According to his forecasts, Russian coal exports this year will be between 190–200 million tons. By the end of 2025, the price of Russian thermal coal could rise to $115–120 per ton, and coking coal to $68 per ton.

Despite the growing «green agenda» in the West, coal remains a fundamental energy source for global electricity generation, steelmaking, and cement industries. This is particularly true for developing countries, where coal remains the most accessible and cost-effective energy source.

According to the Ministry of Energy, by 2030, Russia will be able to export approximately 210 million tons of coal via the Eastern Polygon, and this volume could reach 270 million tons by 2035. This means that Russian miners will be provided with work for many years to come.